International

International  Politics

Politics  Local

Local  Finance

Finance  Sports

Sports  Entertainment

Entertainment  Lifestyle

Lifestyle  Technology

Technology  Literature

Literature  Science

Science  Health

Health  4 hours ago

3

4 hours ago

3

U.S. markets turned lower Tuesday as a semiconductor-led selloff, hawkish Federal Reserve signals, and softer digital assets overwhelmed earlier relief from Middle East diplomacy.

Key Takeaways

- Nasdaq lost nearly 400 points by 10:48 a.m. as Micron led a June 23 chip selloff.

- Fed signals kept pressure on artificial intelligence (AI) valuations, with Warsh’s 2026 dot plot at 3.8%.

- Micron’s June 24 report may test AI memory demand as Iran talks enter 60 days.

At 10:48 a.m. Eastern time on Tuesday, June 23, 2026, the Nasdaq Composite stood at 25,766.67, down 399 points, while the S&P 500 was at 7,413.96, off 58.83 points. The NYSE Composite fell 91.27 points to 23,504.95.

Nasdaq Composite on June 23.

Nasdaq Composite on June 23.The Dow Jones Industrial Average was the outlier, rising 29.77 points to 51,742.48, helped by its lighter exposure to high-growth technology shares.

Chip Weakness Controls the Tape

The pressure followed Monday’s tech-led weakness and intensified as a global semiconductor selloff spread through U.S. trading. Memory chip stocks were hit hard after sharp declines in Asian markets, particularly among Korean memory names, while traders moved cautiously ahead of Micron’s fiscal third-quarter report due Wednesday, June 24.

Micron on June 23, 2026.

Micron on June 23, 2026.The Ishares Semiconductor ETF fell about 6%, with several large chip names under heavy pressure. Micron dropped roughly 8% to 11% intraday, trading around $1,073 to $1,108 after closing Monday at $1,211.38 following an Anthropic supply deal. Intel fell about 7% to 8%, AMD declined about 6%, and Nvidia lost roughly 3%.

The selloff matters because semiconductors sit at the center of the artificial intelligence investment cycle. After a powerful multi-month rally, traders are now testing whether demand for AI infrastructure, memory chips and data center capacity can justify stretched valuations. Micron’s earnings will offer one of the clearest near-term readings on whether AI memory demand remains strong enough to support those expectations.

Fed Stance Adds Another Headwind

The rate backdrop has also turned less friendly for growth stocks. At the June 17 Federal Open Market Committee (FOMC) meeting, the Fed held rates steady at a 3.50% to 3.75% target range, but policymakers raised their year-end 2026 median federal funds rate projection to 3.8%, up from 3.4% in March.

New Fed Chair Kevin Warsh also removed language that had previously pointed toward easier policy and declined to offer traditional forward guidance. His message emphasized inflation control, including a commitment to the Fed’s 2% target after what he called years of misses. That posture has kept rate-hike expectations alive and added pressure to long-duration assets.

Higher rate expectations tend to weigh most on companies whose valuations depend on future earnings growth. That dynamic is especially important for AI and semiconductor stocks, where investors are pricing in years of expansion. When discount rates rise, the market often becomes less forgiving of lofty multiples, heavy capital spending and earnings that depend on future demand.

Digital assets and metals weaken

The risk-off mood extended into digital assets. During the same timeframe, bitcoin stood at $62,451, up 0.30%, but down 3.71% over 24 hours and 4.88% over seven days. Ethereum traded at $1,661, up 0.34% over the last hour, but down 5.26% over 24 hours and 6.62% over seven days.

Precious metals also weakened despite their traditional safe-haven role. Gold was down about 1.4% near $4,145 per ounce, while silver fell more than 4% toward the $62 area. The move reflected a mix of profit-taking, a stronger dollar, and yield pressure, and reduced immediate demand for geopolitical hedges as Middle East talks showed progress.

SpaceX shows relative resilience

SpaceX, trading under SPCX after going public around June 12, remained volatile but showed relative resilience compared with pure-play chip names. The company priced its IPO at $135 per share, raised roughly $75 billion and entered public markets with an initial valuation above $1.75 trillion.

The stock rallied after its debut, reaching above $160 intraday, before pulling back on dilution concerns tied to a $60 billion all-stock acquisition of AI coding startup Cursor. Tuesday’s relative strength suggests investors are still separating some long-term growth narratives, including Starlink and Starship, from the immediate reset hitting memory and chip names.

Geopolitical Relief Remains Incomplete

Middle East diplomacy has helped ease some market pressure, but it has not resolved the conflict risk. On June 17, President Trump and Iranian President Pezeshkian signed the Islamabad Memorandum of Understanding, launching a 60-day diplomatic process aimed at a final war-ending deal. The framework covers hostilities, Lebanon and Hezbollah, the Strait of Hormuz, oil sanctions and reconstruction issues.

On Monday, technical talks in Switzerland produced what Vice President JD Vance called a “very, very good day.” Iran agreed to allow International Atomic Energy Agency inspectors back, a de-confliction cell was established to monitor the Lebanon ceasefire, and discussions continued over keeping the Strait of Hormuz open. On Tuesday, Pezeshkian traveled to Pakistan for follow-up talks with mediators from Qatar and Pakistan.

For markets, the message is clear: geopolitical relief helped earlier, but Tuesday’s trade was dominated by domestic financial conditions and chip-sector stress. Micron’s June 24 report is now the next major test for the AI trade, while the Fed’s hawkish turn raises the bar for any quick rebound in risk assets.

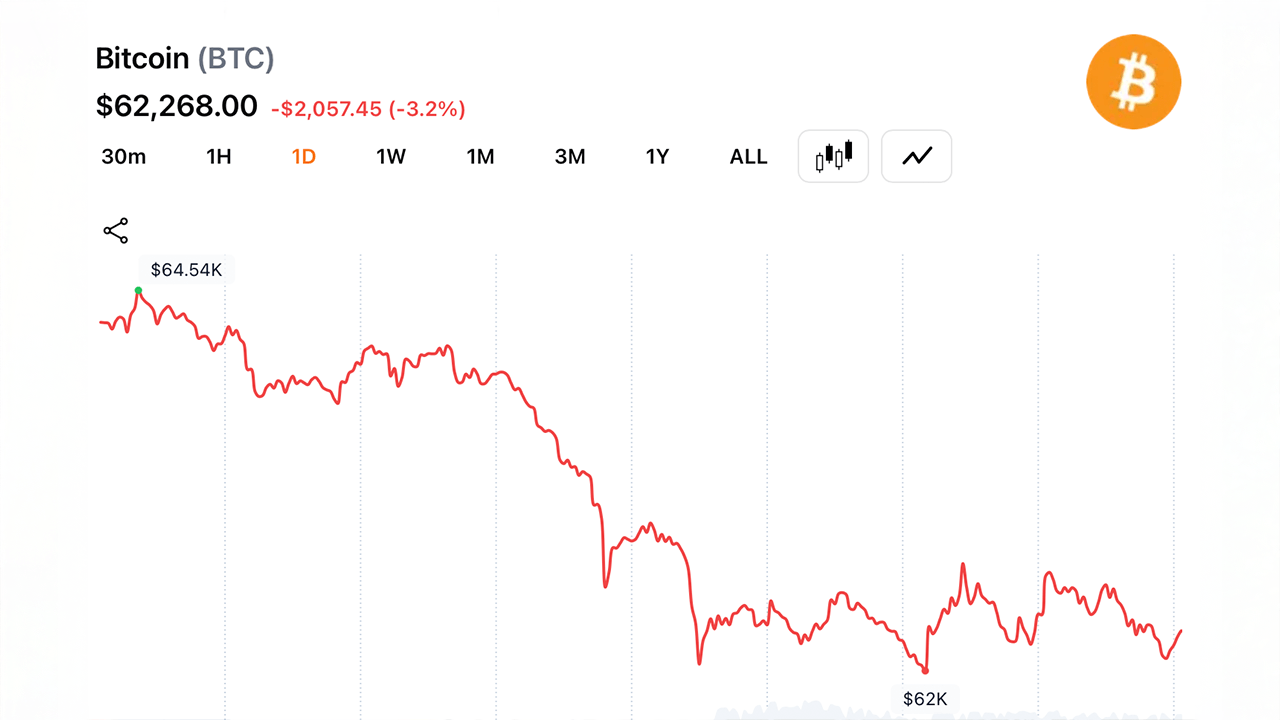

Bitcoin (BTC) traded at $62,309 on June 23, 2026, at 8:30 a.m. Eastern time, holding near the lower edge of…

Bitcoin Sellers Control Volume as $62K Support Faces Its Biggest Test of June

Bitcoin (BTC) traded at $62,309 on June 23, 2026, at 8:30 a.m. Eastern time, holding near the lower edge of…

Bitcoin Sellers Control Volume as $62K Support Faces Its Biggest Test of June

Bitcoin (BTC) traded at $62,309 on June 23, 2026, at 8:30 a.m. Eastern time, holding near the lower edge of…

English (US)

English (US)